Tax Planning for Law Firm Owners — 5 Strategies That Reduce What You Pay the IRS

- Tax Wealth Consultant

- May 8

- 8 min read

Running a law firm in Orange County is one of the most financially complex positions a business owner can be in. As an attorney, you are simultaneously a licensed professional, a business owner, an employer, and in many cases a partner — each role carrying its own set of tax obligations, planning opportunities, and risks. Most law firm owners work with a tax preparer near me who handles the annual return. Far fewer work with a tax specialist near me who is looking at the business structure, compensation design, retirement plan strategy, and income timing decisions that collectively determine how much of what the firm earns actually stays with the partners. Tax planning law firms across Orange County rely on is not a one-time exercise. Tax planning for attorneys who run their own practice requires a fundamentally different approach than general business owner tax planning. It is a year-round process that requires understanding how your entity structure, owner compensation, and retirement contributions interact — and optimizing each one in coordination with the others. This post outlines five specific tax planning strategies that apply to law firm owners and attorneys in Orange County and across California. These are not generic small business tips. They are strategies that apply specifically to the way law practices are structured, how partners and associates are compensated, and how California's state tax rules compound the federal planning picture.

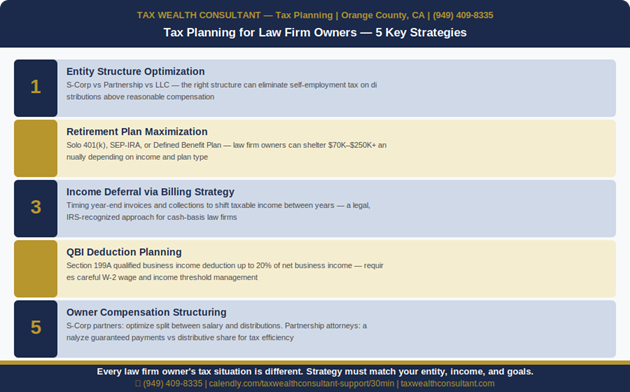

Strategy 1 — Entity Structure and the S-Corporation Election

The most impactful tax planning decision a law firm owner can make is often the one made at formation — or missed at formation and corrected later. The choice between operating as a sole proprietorship, partnership, LLC, or S-corporation determines how self-employment tax applies to your income. For attorneys operating as sole proprietors or single-member LLCs taxed as disregarded entities, every dollar of net income is subject to self-employment tax — 15.3% on the first $176,100 of net earnings in 2026 and 2.9% on everything above that. This is in addition to federal and California income tax. An S-corporation election allows a law firm owner to split income between a reasonable salary — which is subject to payroll taxes — and distributions — which are not. For a California attorney earning $400,000 in net firm income, an appropriately structured S-corporation with a documented reasonable compensation of $150,000 can eliminate payroll tax on the remaining $250,000 in distributions. The tax savings are real, measurable, and recurring year after year. Business owner tax planning that does not address entity structure first is leaving the largest lever on the table. At Tax Wealth Consultant, entity structure review is the first step in every law firm tax planning engagement — because no retirement plan, deduction strategy, or income deferral approach will have as large a compounding impact as the right entity election made and maintained correctly.

Law Firm Tax Strategy Overview — Which Approach Fits Your Situation

The table below summarizes the six most impactful tax planning strategies for law firm owners, who they apply to, and the realistic tax impact of each. Every attorney's situation is different — the right combination depends on your entity, income level, age, and firm structure. A tax specialist near me who understands law firm tax strategy will apply these in coordination, not in isolation.

Strategy | Who It Applies To | Potential Tax Impact |

S-Corp election | Solo attorneys and small firm partners paying self-employment tax | Eliminate SE tax on distributions above reasonable salary — $15K–$30K+ annual savings |

Solo 401(k) or SEP-IRA | Self-employed attorneys with no full-time employees | Up to $70,000 pre-tax contribution annually reduces taxable income dollar for dollar |

Defined Benefit Plan | High-income attorneys 45+ with stable income above $300K | Shelter $100,000–$250,000+ annually — largest available retirement deduction |

QBI deduction (Section 199A) | Pass-through attorneys below income threshold | Up to 20% deduction on qualified business income — requires W-2 wage planning |

Year-end billing deferral | Cash-basis law firms with control over invoice timing | Shift income to following tax year by delaying December invoices — fully IRS-compliant |

Owner compensation split | S-Corp law firm owners | Reduce payroll tax base by optimizing salary vs distribution ratio with documented reasonable comp |

Strategy 2 — Retirement Plan Design for Law Firm Owners

Retirement plan contributions are among the most powerful tax planning tools available to law firm owners — and among the most underutilized. The reason is that most attorneys work with a tax preparer near me who files the return but does not proactively advise on which retirement plan structure maximizes the deduction for their specific income level and firm structure. For a solo attorney or small firm partner with no full-time W-2 employees, a Solo 401(k) allows contributions of up to $70,000 per year in 2026 — combining employee deferrals of up to $23,500 and employer profit-sharing contributions of up to 25% of compensation. Every dollar contributed reduces taxable income dollar for dollar. For a high-income attorney — particularly one earning above $300,000 annually who is 45 or older — a Defined Benefit Plan can shelter $100,000 to $250,000 or more per year, depending on age and income. The annual contribution is calculated actuarially and is fully deductible, making it the most aggressive tax deferral tool available to a self-employed professional under current IRS rules. Law firm tax strategy around retirement plans must also coordinate with entity structure. An S-corporation law firm pays owner-attorneys a salary, and retirement contributions are calculated as a percentage of that salary — which means the reasonable compensation decision directly affects the maximum retirement plan contribution. A tax accountant near me who is running these calculations in coordination can find the combination that minimizes total tax while maximizing retirement savings. At Tax Wealth Consultant, we model the interaction between entity structure, owner salary, and retirement plan contribution limits for every law firm owner we work with — because the numbers change meaningfully when all three variables are optimized together.

Strategy 3 — Income Timing and the QBI Deduction

Two additional law firm tax strategy levers that are frequently missed by attorneys working with a general tax services near me provider are income timing and the Section 199A qualified business income deduction. Income timing applies primarily to cash-basis law firms — which includes most small and mid-size practices. Under cash-basis accounting, income is recognized when collected, not when billed. This gives law firm owners a meaningful degree of control over when income hits their tax return. A law firm that delays sending December invoices until January, or that defers collection of a large settlement fee into the following year, shifts that income into a future period — legally, with IRS recognition, and without deferring the underlying work. This is not tax evasion. It is tax planning Orange County attorneys with cash-basis accounting have available to them every year. The Section 199A deduction — often called the QBI deduction — allows eligible pass-through business owners to deduct up to 20% of qualified business income on their personal tax return. For law firms, which are specifically listed as a specified service trade or business, the deduction begins to phase out above $197,300 of taxable income for single filers and $394,600 for married filers in 2026. Business owner tax planning that keeps taxable income below these thresholds — through retirement plan contributions, timing strategies, or charitable giving — preserves access to a deduction that can be worth $30,000 to $80,000 or more annually for a law firm earning $400,000 to $600,000 in net income. A tax accountant near me who is not monitoring your income against these thresholds throughout the year is likely leaving this deduction on the table.

Is Your Law Firm's Tax Plan Built Around Your Business Structure?

Most law firm owners pay more tax than they should — not because they are doing anything wrong, but because the strategies that reduce their tax bill require coordination between entity structure, owner compensation, retirement plan design, income timing, and the QBI deduction threshold. A tax preparer near me who files the return each spring is not the same as a tax specialist near me who is running these scenarios in Q3 and Q4 of every year and making adjustments before the year closes. Tax planning Orange County law firm owners access at Tax Wealth Consultant is built around your specific entity, income level, and goals. We review your business structure, model the interaction between compensation and retirement contributions, identify income deferral opportunities available under your firm's billing model, and ensure your QBI deduction is protected throughout the year. If you are a law firm owner or attorney in Orange County and want a tax planning strategy that goes beyond the annual return, book a consultation with our team. Call (949) 409-8335 or schedule directly below — and discover exactly what your firm's tax position could look like with the right law firm tax strategy in place.

Frequently Asked Questions — Tax Planning for Law Firm Owners

What are the most important tax planning strategies for law firm owners?

The five most impactful tax planning strategies for law firm owners are: S-corporation entity structure to eliminate self-employment tax on distributions, retirement plan maximization through Solo 401(k) or Defined Benefit Plans, Section 199A QBI deduction planning, income timing through billing deferral on a cash-basis return, and owner compensation structuring. Each strategy interacts with the others — which is why law firm tax strategy requires coordination across all five, not just one at a time. Tax planning Orange County law firm owners access through Tax Wealth Consultant covers all five levers. S corporation tax planning is the foundation of law firm tax strategy. S corporation tax planning done correctly eliminates thousands in annual self-employment tax — because it has the largest recurring impact. Tax planning law firms need is different from general tax services near me — it requires someone who understands law firm billing, partner compensation, and California entity rules. Tax planning for attorneys at every income level is what we do.

Should my law firm be an S-corporation?

For many law firm owners in Orange County, an S-corporation election is the highest-impact tax planning decision available. It allows the owner to pay a reasonable salary — subject to payroll taxes — and take additional income as distributions, which are not subject to self-employment tax. For an attorney earning $300,000 to $600,000 in net firm income, the annual payroll tax savings can be $15,000 to $40,000 or more. Whether an S-corporation is the right structure depends on your income level. S corporation tax planning for California-based attorneys must also account for the California LLC fee structure, the number of partners, California franchise tax, and other factors — which is why business owner tax planning should start with a structure review. Contact Tax Wealth Consultant at (949) 409-8335 to discuss your situation.

How much can a law firm owner contribute to a retirement plan?

A law firm owner's retirement plan contribution limit depends on the plan type and income. With a Solo 401(k), the 2026 limit is $70,000 — combining employee deferrals of $23,500 and employer contributions of up to 25% of compensation. A SEP-IRA allows contributions of up to 25% of net self-employment income. For high-income attorneys 45 and older, a Defined Benefit Plan can shelter $100,000 to $250,000 or more annually. Tax planning for attorneys includes retirement plan selection as a core component. Tax planning law firms do correctly always models retirement plan limits against entity structure. Tax services near me that are construction-accounting focused will not know these rules — you need a tax specialist near me who understands law firm tax strategy to model which plan maximizes your deduction given your entity structure, compensation level, and retirement timeline.

What is the QBI deduction and does it apply to law firm owners?

The Section 199A qualified business income deduction allows eligible pass-through business owners — including law firm owners — to deduct up to 20% of net business income on their personal tax return. Law firms are classified as a specified service trade or business, which means the deduction phases out above $197,300 of taxable income for single filers and $394,600 for joint filers in 2026. Business owner tax planning that keeps income below these thresholds — through retirement contributions, income deferral, or other strategies — can preserve a deduction worth $30,000 to $80,000 or more annually. A tax accountant near me who monitors your income against these thresholds throughout the year is essential to protecting this deduction.

Does Tax Wealth Consultant provide tax planning for law firms in Orange County?

Yes. Tax Wealth Consultant provides tax planning for law firm owners and attorneys throughout Orange County and Southern California. Our services include entity structure review, retirement plan design, QBI deduction optimization, income timing strategy, and year-round business owner tax planning — not just annual tax preparation. We work with solo attorneys, small firm partners, and growing practices at every stage. Call us at (949) 409-8335 or book a consultation at calendly.com/taxwealthconsultant-support/30min to discuss your firm's tax position.

Comments