How to Use S-Corp Structure for Tax Planning in 2026 — Reasonable Compensation, Defined Benefit Plans, Profit Sharing, and the Levers That Work

- Tax Wealth Consultant

- Jun 9

- 12 min read

In our prior guides we walked through the facts of C-Corp vs S-Corp taxation, the strategic reasons high-bracket business owners sometimes elect C-Corp, the strict S-Corp qualifications under IRC §1361, and a side-by-side comparison of both entities. This guide walks through the planning side of S-Corp ownership — how business owners who already operate as S-Corps use the structure for tax planning. The S-Corp election by itself does not save tax. The planning levers built on top of the S-Corp structure are what produce the actual tax savings.

Five major levers drive S-Corp tax planning in 2026: (1) the pass-through structure that lets owners avoid double taxation S-Corp owners face when distributing C-Corp earnings; (2) reasonable compensation optimization that produces S-Corp self employment tax savings on the non-wage portion of profit; (3) Solo 401(k) and S-Corp profit sharing plan contributions that shelter substantial income under IRS Notice 2025-67 limits; (4) S-Corp defined benefit plan structures for high-income owners that allow contributions far above defined contribution limits; (5) the QBI deduction Section 199A — made permanent under OBBBA 2025 — that further reduces the effective rate on pass-through income. Every fact below comes directly from the Internal Revenue Code, IRS publications, IRS Notice 2025-67 (2026 cost-of-living adjustments), or verified federal case law.

Important honesty boundary: this article describes S-Corp tax planning strategies for business owners who have legitimately elected S-Corp status under IRC §1361 and meet all qualification requirements. None of the strategies below licenses underpaying a shareholder-employee's reasonable compensation. The Watson v. Commissioner decision and the IRS Fact Sheet FS-2008-25 standards govern compensation — they are not optional. The S-Corp tax planning levers covered below build on TOP of properly-paid reasonable compensation, not in place of it.

Avoid Double Taxation — The Foundation of S-Corp Tax Planning

The starting point of S-Corp tax planning is the structural avoidance of double taxation. Under Subchapter S (IRC §§1361-1379), an S-Corp generally pays NO federal income tax at the entity level. All ordinary business income, deductions, and credits flow through to shareholders via Schedule K-1 (Form 1120-S) and are reported once on the shareholders' personal Form 1040 returns under IRC §1366. There is no second layer of dividend tax when after-tax profits are distributed.

HOW AVOID DOUBLE TAXATION S-CORP STRUCTURE COMPARES TO C-CORP

C-Corp profit of $100: corporate-level 21% tax = $21, leaving $79. Distribution of $79 as qualified dividend taxed at up to 23.8% (20% + 3.8% NIIT for high earners) = $18.80 second-layer tax. Combined federal tax: $39.80 on $100

S-Corp profit of $100: $0 entity-level tax. $100 of pass-through income flows to shareholder's Form 1040 at individual rates. If shareholder is in 37% top bracket: $37 federal tax. Combined federal tax: $37 on $100

With QBI deduction Section 199A (covered in Section 5): effective rate on the S-Corp side drops to roughly 29.6% — significantly below the combined C-Corp + dividend rate

This single-layer-of-tax structure is the foundation that every other S-Corp tax planning lever builds on. The pass-through mechanism also means S-Corp shareholder distributions of after-tax profits are generally NOT taxable when received — they reduce stock basis under IRC §1368 but produce no additional tax (unless distributions exceed basis, in which case the excess is treated as capital gain). S-Corp shareholder distributions in excess of stock basis are reported on the shareholder's personal return as a capital gain under IRC §1368(b)(2) — making basis tracking critical to defer or minimize tax on S-Corp shareholder distributions. This is fundamentally different from a C-Corp dividend, which is taxable on receipt regardless of corporate-level tax already paid (source: IRC §1366; IRC §1368; IRS Instructions for Form 1120-S).

Reasonable Compensation — The Most Powerful S-Corp Self Employment Tax Savings Lever

The single largest S-Corp tax planning advantage for owner-operators is the difference in payroll tax treatment between salary and distribution. Wages paid to a shareholder-employee are subject to FICA (Social Security and Medicare) — 15.3% combined employer/employee share, up to the 2026 Social Security wage base of $184,500. Distributions from the S-Corp's after-tax profits are NOT subject to FICA, self-employment tax, or any payroll tax. This is the structural source of S-Corp self employment tax savings (source: IRC §1366; IRC §3121; IRS Fact Sheet FS-2008-25).

Every S-Corp shareholder-employee who performs services for the corporation faces a single optimization question: how much of the total economic return should be paid as W-2 wages (subject to FICA) versus how much should be paid as distributions (not subject to FICA)? The answer must respect IRS reasonable compensation requirements — but within those requirements, the answer materially changes the tax bill.

Consider an S-Corp generating $200,000 of net business income, with a single shareholder-employee performing all services. Scenario A — entirely as wages: $200,000 W-2 wages × 15.3% combined FICA up to Social Security wage base of $184,500 + 2.9% Medicare on the excess = approximately $28,213 in payroll taxes. Scenario B — $80,000 reasonable compensation as wages + $120,000 as distributions: $80,000 × 15.3% = $12,240 in payroll taxes. Annual S-Corp self employment tax savings: approximately $15,973. (Illustrative federal calculation; actual results vary based on industry, geography, services performed, state rules, and shareholder facts.)

In Watson v. United States, 668 F.3d 1008 (8th Cir. 2012), a CPA shareholder paid himself $24,000 in salary while taking distributions exceeding $200,000. The 8th Circuit upheld the IRS's reclassification of approximately $67,044 per year as additional wages subject to payroll tax. The Watson case is the leading federal authority on S-Corp reasonable compensation — the lesson is that S-Corp self employment tax savings are real and significant when the salary is reasonable, but artificially low salaries trigger recharacterization plus penalties and interest. The IRS factors for reasonable compensation are listed in IRS Fact Sheet FS-2008-25 and include training and experience, duties and responsibilities, time devoted to the business, comparable salaries at similar businesses, dividend history, and the use of formulas — none of which permit a $24,000 salary on $200,000+ of services-based income.

S-Corp Solo 401(k) and S-Corp Profit Sharing Plan — Sheltering Up to $72,000 in 2026

Once S-Corp reasonable compensation is set at the right level, the next major S-Corp tax planning lever is the retirement plan contribution. A Solo 401(k) — sometimes structured to include a profit sharing plan component — allows an S-Corp shareholder-employee to make TWO types of contributions in the same year: an employee deferral AND an employer contribution. The combined total reaches the IRC §415(c) annual additions limit of $72,000 for 2026, per IRS Notice 2025-67.

S-CORP SOLO 401(k) — 2026 LIMITS UNDER IRS NOTICE 2025-67

Employee elective deferral: up to $24,500 (IRC §402(g)) — must come from W-2 wages

Catch-up contribution age 50+: additional $8,000 — total elective deferral $32,500

Super-catch-up ages 60-63: additional $11,250 — total elective deferral $35,750

Employer contribution (S-Corp profit sharing plan component): up to 25% of W-2 wages

Combined annual additions limit: $72,000 (IRC §415(c)(1)(A)) — or $80,000 with catch-up — or $83,250 for ages 60-63

Annual compensation limit: $360,000 (IRC §401(a)(17)) — earnings above this are not counted for employer contribution calculation

Because the employer contribution under a Solo 401(k) is capped at 25% of W-2 wages, the S-Corp reasonable compensation amount directly determines how much can be contributed as the employer match. A $50,000 W-2 supports a maximum $12,500 employer contribution. A $190,000 W-2 supports the full $47,500 employer contribution needed to combine with the $24,500 elective deferral and reach the $72,000 ceiling. This means optimization of S-Corp reasonable compensation is not just a payroll-tax question — it is

also a retirement-contribution question. Setting compensation too low reduces retirement plan capacity; setting it too high wastes the FICA savings advantage that drove the S-Corp election in the first place (source: IRC §401(a)(17); IRC §415(c); IRC §402(g); IRS Notice 2025-67).

CONTRIBUTION TIMING — TWO DIFFERENT DEADLINES

Employee elective deferrals MUST be made by December 31 of the plan year — coming out of W-2 paychecks during the year

Employer contributions (S-Corp profit sharing plan) can be made up to the corporation's tax return filing deadline including extensions — generally September 15 of the following year for calendar-year S-Corps

The S-Corp profit sharing plan must be ESTABLISHED by December 31 of the plan year, even if the contribution itself is funded later (source: IRC §404; IRS Publication 560)

S-Corp Defined Benefit Plan — Where High-Income S-Corp Owners Capture the Largest Contributions

For high-income S-Corp owners whose retirement planning capacity exceeds the $72,000 defined contribution limit, the S-Corp defined benefit plan is the next planning lever. A defined benefit plan is governed by IRC §415(b) and is structured to fund a target annual retirement benefit, with annual contributions determined by an actuarial calculation based on the participant's age, current compensation, and the target benefit at retirement. The IRC §415(b)(1)(A) annual benefit limit for 2026 is $290,000, increased from $280,000 in 2025 per IRS Notice 2025-67.

S-CORP DEFINED BENEFIT PLAN — 2026 STRUCTURE

Maximum annual benefit at retirement: $290,000 per year (IRC §415(b)(1)(A); IRS Notice 2025-67)

Compensation cap on annual contribution calculations: $360,000 (IRC §401(a)(17))

Annual contribution determined by actuarial valuation — depends on age, current W-2 compensation, and target benefit

Older participants with stable high income typically support the largest annual contributions — often $100,000 to $300,000+ per year

S-Corp defined benefit plan contributions are based on W-2 compensation, NOT on K-1 pass-through income — meaning W-2 wages must be high enough to support the actuarial calculation

Defined benefit contributions are 100% employer-funded — they are deductible at the S-Corp level and reduce pass-through income to shareholders

A high-income S-Corp owner can combine an S-Corp defined benefit plan with a Solo 401(k) profit sharing plan to maximize total annual contributions. When combined plans are in place, the 25% deduction limit under IRC §404(a)(7) applies to the combined employer contributions. The defined benefit plan contribution is typically the larger component, with the Solo 401(k) employee deferral added on top. Combined annual deductible contributions for an older high-income shareholder can reach $300,000+ in some fact patterns. (Source: IRC §415; IRC §404(a)(7); IRS Publication 560; IRS Notice 2025-67.)

S-CORP DEFINED BENEFIT PLAN CRITICAL CONSIDERATIONS

Defined benefit plans REQUIRE consistent annual funding — they are not discretionary like profit sharing plans

Annual actuarial valuation is required — and adds administrative cost

Plan typically must be maintained for at least 3-5 years to avoid IRS recharacterization risk

Adding non-shareholder employees triggers nondiscrimination testing — and may require contributions for those employees

Plan must be properly established (typically through a third-party administrator) before December 31 of the plan year

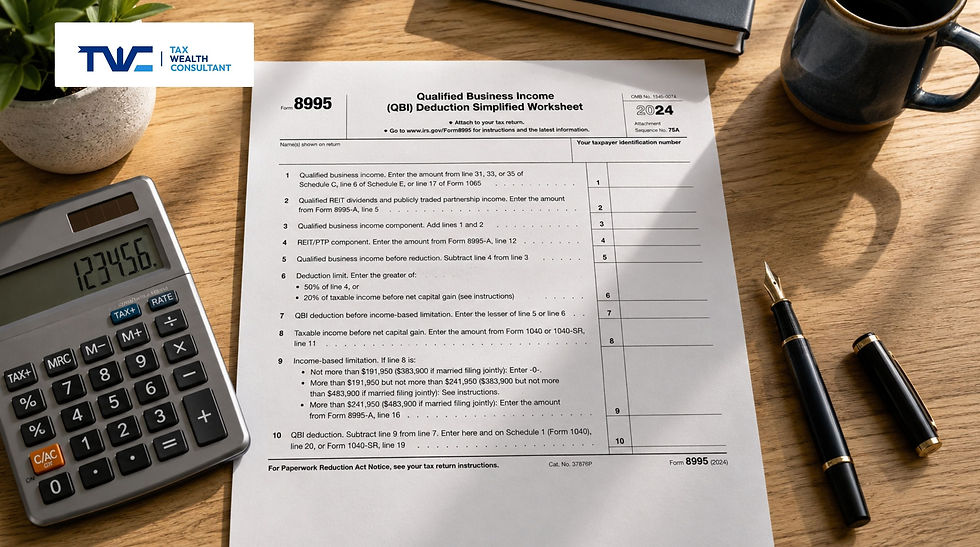

QBI Deduction Section 199A — Permanent Under OBBBA, 20% on Pass-Through Income

The QBI deduction Section 199A is a 20% deduction on qualified business income from pass-through entities, including S-Corps. The deduction was originally enacted in TCJA 2017 with a scheduled sunset — the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made the QBI deduction Section 199A PERMANENT under current law. C-Corps are NOT eligible for the QBI deduction Section 199A. This is a structural advantage of pass-through entities that does not exist for C-Corps regardless of how they are managed (source: IRC §199A; OBBBA 2025).

QBI DEDUCTION SECTION 199A MECHANICS FOR S-CORP SHAREHOLDERS

Deduction: up to 20% of "qualified business income" (QBI) from the S-Corp, claimed on the shareholder's personal Form 1040 via Form 8995 or Form 8995-A

QBI generally equals the S-Corp's ordinary business income passed through to the shareholder — but excludes capital gains, dividends, interest income, and reasonable compensation paid to the shareholder

Income thresholds for 2026: full deduction available below $201,750 (single) / $403,500 (MFJ); phase-out range above these thresholds

Above the threshold, the deduction may be limited based on W-2 wages paid by the S-Corp and qualified property basis

Specified Service Trade or Business (SSTB) limitations apply above the threshold — services in health, law, accounting, consulting, financial services, and certain other fields face deduction phase-out

For a high-bracket S-Corp shareholder eligible for the full QBI deduction Section 199A, the effective federal marginal rate on S-Corp pass-through income drops from 37% to approximately 29.6% (37% × 80%). The QBI deduction Section 199A is not a separate filing — it is a calculation on Form 8995 or 8995-A that is built into the shareholder's individual return. For S-Corp owners above the income threshold, the W-2 wages paid by the S-Corp affect the QBI deduction Section 199A calculation — which creates another optimization consideration alongside reasonable compensation and retirement plan funding.

Coordinating S-Corp Tax Planning — The Five Levers Interact

The five S-Corp tax planning levers above — pass-through structure, reasonable compensation, Solo 401(k)/profit sharing, defined benefit plan, and QBI deduction Section 199A — do not work independently. They interact, and the choice of one lever affects the others. S-Corp tax strategy 2026 requires multi-lever coordination, not single-lever optimization.

HOW THE LEVERS INTERACT

Setting REASONABLE COMPENSATION TOO LOW reduces Solo 401(k) employer contribution capacity (which is 25% of W-2 wages) and triggers IRS recharacterization risk under Watson

Setting REASONABLE COMPENSATION TOO HIGH wastes the FICA savings advantage of pass-through distributions, increasing total payroll tax exposure

Adding an S-CORP DEFINED BENEFIT PLAN typically requires higher W-2 compensation to support the actuarial calculation — pushing reasonable compensation higher than the FICA-optimal level

For shareholders above the QBI deduction Section 199A income threshold, paying more in W-2 wages can INCREASE the QBI deduction available on remaining pass-through income — creating a counter-balancing optimization

Defined contribution and defined benefit plan contributions reduce pass-through income, which reduces QBI subject to the §199A deduction — but the income tax deduction from retirement contributions typically more than offsets the lost QBI deduction value

Because the levers interact, the optimal S-Corp tax planning structure is fact-specific and must be modeled. A 45-year-old S-Corp shareholder with $300,000 of profit and a desire to reach the Solo 401(k) cap has different optimal compensation than a 60-year-old with $600,000 of profit and capacity for an S-Corp defined benefit plan. The same shareholder's optimal compensation changes year-to-year as business profit fluctuates and as IRS limits adjust (the 2026 limits in this guide are inflation-adjusted from 2025 per IRS Notice 2025-67, and the 2027 limits will adjust again). This is exactly the kind of multi-variable optimization a tax planning firm Irvine business owners trust runs each year for S-Corp clients.

What This Guide Does Not Cover

This guide describes the major federal S-Corp tax planning levers available in 2026. It does NOT cover: (1) whether S-Corp election is the right entity choice for your specific business — see our C-Corp vs S-Corp facts and comparison guides; (2) the IRC §1361 qualifications and limitations that must be maintained for the S-Corp election to remain valid — covered in our S-Corp qualifications guide; (3) the specific reasonable compensation amount appropriate for your industry, location, role, and time devoted — that determination requires personal review of comparable salaries and the IRS Fact Sheet FS-2008-25 factors; (4) the actuarial calculation for an S-Corp defined benefit plan, which requires a qualified third-party administrator; (5) nondiscrimination testing for defined benefit and defined contribution plans when the S-Corp has non-shareholder employees; (6) state-level tax planning — California, for example, imposes a 1.5% franchise tax on S-Corp net income that interacts with these planning levers differently than federal-only planning would suggest; (7) the Accountable Plan reimbursement strategy, which is covered in a separate TWC guide; (8) advanced strategies including ESOPs, family member compensation planning, and S-Corp/holding-company structures. Each of these requires personal analysis.

Where to Go From Here

If you operate as an S-Corp and you have not modeled all five S-Corp tax planning levers under your specific 2026 facts — reasonable compensation, Solo 401(k)/profit sharing, S-Corp defined benefit plan capacity, QBI deduction Section 199A optimization, and distribution timing — you are almost certainly leaving tax planning value on the table. Tax Wealth Consultant is an Enrolled Agent tax planning firm Irvine based, serving S-Corp owners across Orange County and California. Our team runs the multi-lever S-Corp tax strategy 2026 model under your specific projected profit, age, retirement goals, and state tax exposure — documenting reasonable compensation against Watson v. U.S. standards and IRS Fact Sheet FS-2008-25 factors, sizing Solo 401(k) and S-Corp profit sharing plan contributions, evaluating S-Corp defined benefit plan capacity under IRC §415(b), and coordinating the QBI deduction Section 199A calculation. This is exactly the kind of integrated planning that a tax planning firm Irvine business owners trust delivers each year.

Related:

Sources cited in this article: • Internal Revenue Code §199A — Qualified Business Income deduction (made permanent by OBBBA 2025) • Internal Revenue Code §401(a)(17) — Annual compensation limit ($360,000 for 2026) • Internal Revenue Code §402(g) — Elective deferral limit ($24,500 for 2026) • Internal Revenue Code §404 — Deduction for employer contributions to qualified plans • Internal Revenue Code §404(a)(7) — Combined plan deduction limit • Internal Revenue Code §415(b)(1)(A) — Defined benefit plan annual benefit limit ($290,000 for 2026) • Internal Revenue Code §415(c)(1)(A) — Defined contribution annual additions limit ($72,000 for 2026) • Internal Revenue Code §1361 — S Corporation defined • Internal Revenue Code §1366 — Pro rata allocation of S-Corp items • Internal Revenue Code §1368 — S-Corp distribution rules • Internal Revenue Code §3121 — FICA wage definition • IRS Notice 2025-67 — 2026 cost-of-living adjustments for retirement plans (issued November 13, 2025) • IRS Publication 560 — Retirement Plans for Small Business • IRS Form 1120-S — U.S. Income Tax Return for an S Corporation • IRS Schedule K-1 (Form 1120-S) — Shareholder's Share of Income • IRS Form 8995 / 8995-A — QBI Deduction (Simplified / Standard) • IRS Fact Sheet FS-2008-25 — Wage Compensation for S Corporation Officers • One Big Beautiful Bill Act (OBBBA), P.L. 119-21 (signed July 4, 2025) • Watson v. United States, 668 F.3d 1008 (8th Cir. 2012) — S-Corp reasonable compensation • Revenue Ruling 74-44 — S-Corp shareholder compensation |

Want a Real S-Corp Tax Planning Model for Your Business?

Tax Wealth Consultant runs the integrated S-Corp tax planning model under your specific facts — reasonable compensation against Watson standards, Solo 401(k) and S-Corp profit sharing plan sizing, S-Corp defined benefit plan capacity, QBI deduction Section 199A optimization, and distribution timing. We model the levers together over multiple years and document the strategy in a defensible memo. No sales pitch — just a real analysis.

Or call (949) 409-8335 — speak with an Enrolled Agent Irvine today

Or email support@taxwealthconsultant.com

Comments