S-Corp Qualifications and Limitations for 2026 — The IRS Rules on Shareholders, K-1 Distributions, and Reasonable Compensation

- Tax Wealth Consultant

- Jun 7

- 12 min read

The S Corporation is one of the most common entity choices for small and mid-sized business owners — but it is also the entity structure with the strictest IRS eligibility rules. Unlike a C Corporation, which has effectively no shareholder restrictions, an S-Corp must satisfy a set of detailed qualifications under Internal Revenue Code Section 1361 — and any violation of those qualifications, even an inadvertent one, can automatically terminate S-Corp status and revert the corporation to default C-Corp taxation. Understanding the S-Corp qualifications and limitations is therefore not optional for any business owner already operating as an S-Corp or considering electing S-Corp status.

This guide is a facts-only reference. We walk through what the IRS rules actually say about S-Corp qualifications, the S-Corp eligibility requirements under IRC Section 1361, the S-Corp 100 shareholder limit and family-aggregation rules, the S-Corp shareholder requirements (US citizens and resident aliens only — S-Corp nonresident alien shareholder is a statutory disqualifier), the S-Corp one class of stock requirement, the Form 2553 election deadline rules, the mechanics of pro rata share S-Corp income allocation on Schedule K-1 Form 1120-S, and the S-Corp reasonable compensation requirement enforced through the landmark Watson v. Commissioner decision. Every fact below comes directly from the Internal Revenue Code, official IRS publications, IRS forms, or verified federal case law current for 2026.

What Is an S Corporation Under IRC Section 1361?

An S Corporation is a corporation that has made a valid federal tax election to be taxed under Subchapter S of the Internal Revenue Code (IRC §§1361-1379). The S-Corp election does NOT change the underlying legal entity — the business remains a corporation under state corporate law — it only changes how the IRS taxes the business federally. Under Subchapter S, the corporation generally pays no federal income tax at the entity level; instead, all income, deductions, credits, and other tax items pass through to shareholders on Schedule K-1 Form 1120-S and are reported on the shareholders' personal tax returns (source: IRC §1361; IRC §1366; IRS Instructions for Form 1120-S).

The defining statute is IRC Section 1361, which defines an "S corporation" as a "small business corporation" for which an S election is in effect. The term "small business corporation" is itself defined in IRC §1361(b) — and despite the name, the definition has nothing to do with revenue or asset size. "Small business corporation" simply means a corporation that meets all of the S-Corp eligibility requirements covered in the next sections. A corporation with $50 million in revenue can be an S-Corp if it meets the requirements; a corporation with $50,000 in revenue cannot be an S-Corp if it fails any of them.

The S-Corp qualifications and limitations under IRC Section 1361 fall into five main categories: (1) the corporation must be a domestic entity; (2) the S-Corp 100 shareholder limit must not be exceeded; (3) the S-Corp shareholder requirements must be met for every shareholder; (4) the S-Corp one class of stock requirement must be maintained; (5) the corporation must not be an "ineligible corporation" under IRC §1361(b)(2). Violation of any of these requirements at any time during the tax year automatically terminates S-Corp status — there is no IRS notice, no warning, and generally no opportunity to cure the violation without IRS relief under Rev. Proc. 2013-30 (source: IRC §1361(b); IRS Instructions for Form 2553).

S-Corp Shareholder Requirements — Who Can and Cannot Own S-Corp Stock

The S-Corp shareholder requirements are the most heavily-tested area of S-Corp compliance because every change in shareholder composition is a potential violation of IRC §1361(b)(1)(B). Two separate rules apply: a HEAD-COUNT rule (the S-Corp 100 shareholder limit) and an IDENTITY rule (only certain types of shareholders are eligible).

An S-Corp may have NO MORE than 100 shareholders at any time. Exceeding 100 shareholders, even for a single day, automatically terminates S-Corp status. Two important rules soften the limit:

FAMILY AGGREGATION (IRC §1361(c)(1)): All members of a family, including the common ancestor and up to six generations of lineal descendants (plus current and former spouses of any of them), can elect to be counted as ONE shareholder for purposes of the 100-shareholder limit

Spouses also count as one shareholder under the same provision, regardless of whether they elect family aggregation

Note: family aggregation applies to the 100-shareholder COUNT, not to the substantive tax allocations — each individual family member still receives a separate Schedule K-1 Form 1120-S based on their actual ownership

Only the following types of persons or entities may be S-Corp shareholders:

U.S. citizens (including U.S. citizens residing abroad)

U.S. resident individuals (resident aliens for income tax purposes)

Estates of deceased shareholders (limited duration permitted)

Certain qualified trusts: grantor trusts, voting trusts, Qualified Subchapter S Trusts (QSSTs) electing under IRC §1361(d), Electing Small Business Trusts (ESBTs) electing under IRC §1361(e)

Certain tax-exempt organizations — IRC §501(c)(3) charitable organizations and IRC §401(a) qualified retirement plans, subject to unrelated business taxable income (UBTI) rules

The following CANNOT be S-Corp shareholders. Ownership by any one of them automatically terminates S-Corp status:

S-Corp nonresident alien shareholder — IRC §1361(b)(1)(C) explicitly disqualifies any corporation with a nonresident alien shareholder. This is the most common inadvertent termination trigger, often occurring when a U.S. resident shareholder loses resident status or transfers stock to a foreign family member

Partnerships and LLCs taxed as partnerships

C Corporations and other S Corporations (with limited exceptions for QSubs under IRC §1361(b)(3))

Most types of foreign trusts

IRAs and most other types of retirement accounts (with the §401(a) exception above)

The practical implications of these S-Corp shareholder requirements are significant. A green-card-holding shareholder who moves abroad and loses U.S. resident status terminates the S-Corp's election automatically. A shareholder who transfers stock to a foreign relative through inheritance creates an immediate S-Corp nonresident alien shareholder violation. A shareholder who places S-Corp stock in a non-qualifying trust terminates the election. Each of these situations requires either prevention (proper shareholder agreement restrictions on transfers) or remediation under IRS late-relief procedures (source: IRC §1361(b); Rev. Proc. 2013-30; Rev. Proc. 2022-19).

The S-Corp One Class of Stock Rule — IRC §1361(b)(1)(D)

The S-Corp one class of stock rule requires that an S Corporation have only ONE class of stock issued and outstanding. The rule, under IRC §1361(b)(1)(D), is one of the most easily violated S-Corp qualifications because it can be triggered not only by explicit stock structure but also by certain operational decisions that have the EFFECT of creating a second economic class.

WHAT THE ONE CLASS OF STOCK RULE PERMITS

Differences in VOTING rights are explicitly permitted — voting common and non-voting common are treated as one class of stock under Treas. Reg. §1.1361-1(l)(1)

Different identities of shareholders, different basis of shareholders, different timing of stock issuance — none of these create a second class

Bona fide shareholder loans documented with written notes, stated interest, and a fixed repayment schedule — generally treated as debt, not as a second class of stock

WHAT THE ONE CLASS OF STOCK RULE PROHIBITS

Differences in DISTRIBUTION rights — all shares must have identical rights to receive distributions

Differences in LIQUIDATION rights — all shares must have identical rights to assets upon liquidation

Preferred stock paying a fixed dividend ahead of common — creates a second economic class

Disproportionate distributions to shareholders (paying one shareholder $50,000 while paying another shareholder $20,000 when they own equal shares) — can be interpreted as creating a second class of stock

Undocumented "shareholder loans" without notes, interest, or repayment terms — IRS may recharacterize as a second class of stock (Glass Blocks Unlimited v.

The single most common practical violation of the S-Corp one class of stock rule is disproportionate distributions. When shareholders agree informally to distribute corporate profits in some pattern other than strict pro rata, the IRS can interpret the distribution pattern as evidence that the shares have different economic rights, terminating S-Corp status. The safe-harbor practice is to make ALL distributions strictly pro rata to ownership percentage — if Shareholder A owns 60% and Shareholder B owns 40%, every distribution must be 60/40 (source: Treas. Reg. §1.1361-1(l); Glass Blocks Unlimited v. Commissioner; T.C. Memo 2013-180).

Form 2553 Election Deadline and Process

A corporation becomes an S-Corp only by filing a valid Form 2553 (Election by a Small Business Corporation) with the IRS. Until Form 2553 is filed and accepted, a corporation is taxed as a C-Corp by default. The Form 2553 election deadline rules are strict and the consequences of missing the deadline are significant (source: IRC §1362; IRS Instructions for Form 2553).

FORM 2553 ELECTION DEADLINE — IRC §1362(b)

The election must be filed by the 15th day of the 3rd month of the tax year for which the election is to be effective

For calendar-year corporations: Form 2553 election deadline is March 15

Alternative: Form 2553 may be filed at any time during the preceding tax year for the election to take effect the following year

New corporations: Form 2553 must be filed within 2 months and 15 days of the date the corporation begins to do business, acquires assets, or issues stock — whichever is earliest

FORM 2553 SIGNATURE AND CONSENT REQUIREMENTS

Form 2553 must be signed by an authorized corporate officer (president, vice president, treasurer, assistant treasurer, chief accounting officer, or other officer authorized to sign)

Every shareholder at the time of the election must consent in writing — signatures on Form 2553 itself or on a separate attached statement

Spouses with community property interests in the stock must also consent

If even one required shareholder consent is missing, the election fails — it is not partially effective

If a corporation fails to file Form 2553 by the deadline, late election relief may be available under Rev. Proc. 2013-30. The corporation must demonstrate: (1) reasonable cause for the failure; (2) the corporation has been operating as if the election were valid (filing Form 1120-S, issuing K-1s, etc.); (3) all shareholders have reported income consistently with S-Corp treatment; and (4) the request is made within 3 years and 75 days of the intended effective date. Late relief is not automatic — it is granted at IRS discretion based on the facts.

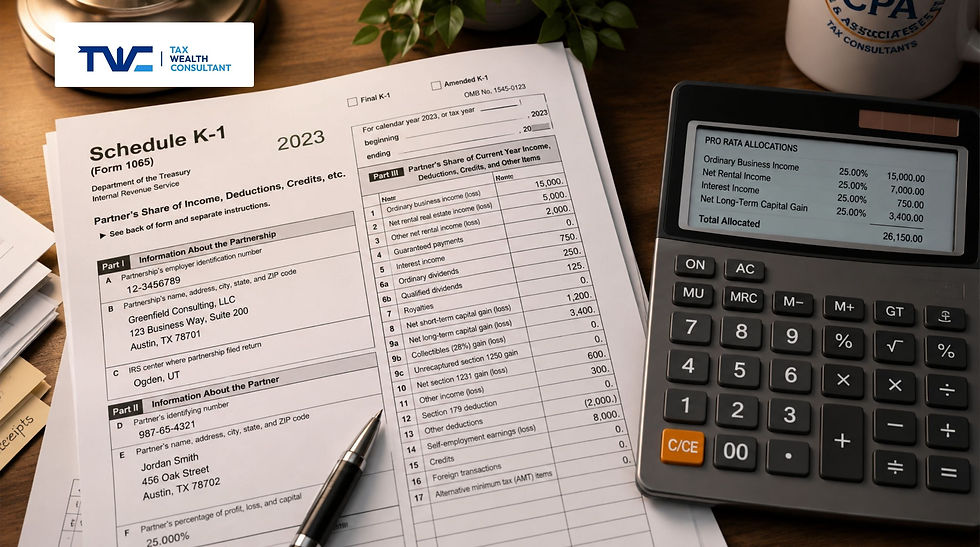

How K-1 Distribution Actually Works — Pro Rata Share S-Corp Allocation

The mechanics of how S-Corp income reaches shareholders is one of the most misunderstood areas of S-Corp taxation. The critical concept is that pro rata share S-Corp allocation under IRC §1366 happens regardless of whether the corporation actually distributes cash to shareholders. The S-Corp is required to allocate income, deductions, and credits to each shareholder on Schedule K-1 Form 1120-S based on the shareholder's proportional ownership — and the shareholder is required to report and pay tax on that allocated income whether or not any cash was received.

HOW PRO RATA SHARE S-CORP ALLOCATION WORKS

Each item of S-Corp income, deduction, and credit is allocated to shareholders based on their pro rata share of stock ownership during the year

If a shareholder owns 25% of the S-Corp for the entire year and the S-Corp has $400,000 of ordinary business income, the shareholder is allocated $100,000 and reports $100,000 on Schedule K-1 Form 1120-S — regardless of whether any cash was distributed

Mid-year ownership changes use per-day allocation under default rules, or alternative "interim closing of the books" methods if all affected shareholders consent

Allocated income increases the shareholder's stock basis under IRC §1367; cash distributions decrease stock basis (and may produce capital gain if distributions exceed basis under IRC §1368)

Each S-Corp shareholder must receive a Schedule K-1 Form 1120-S by the corporation's filing deadline (March 15 for calendar-year corporations, or the extended date if applicable). The Schedule K-1 reports each shareholder's pro rata share of every separately stated item, including: ordinary business income or loss (Box 1); net rental real estate income (Box 2); interest income (Box 4); dividend income (Box 5); royalties (Box 6); short-term and long-term capital gains (Boxes 7-8); Section 179 deduction (Box 11); charitable contributions; other deductions and credits.

The most consequential implication of the pro rata share S-Corp allocation rule is what tax practitioners call "phantom income" — the situation where a shareholder is allocated taxable income but receives no cash distribution to pay the tax. This commonly occurs when an S-Corp retains earnings for reinvestment or debt service. The Tax Court has consistently held that allocated S-Corp income is taxable regardless of distribution status (source: IRC §1366; IRC §1367; IRC §1368; Brooks v. Commissioner, T.C. Memo 2024-77; IRS Instructions for Schedule K-1 Form 1120-S).

S-Corp Reasonable Compensation — The Audit Risk That Drives 1120-S Cases

The S-Corp reasonable compensation requirement is the single largest IRS audit risk in S-Corp taxation. When an S-Corp shareholder also performs services for the corporation (which is the case for almost every closely-held S-Corp), IRS guidance under Rev. Rul. 74-44 and Rev. Rul. 59-221 requires the corporation to pay that shareholder-employee a reasonable salary subject to payroll tax BEFORE making any non-wage distributions. Distributions cannot replace reasonable wages (source: IRS Fact Sheet FS-2008-25; IRS, S Corporation Employees, Shareholders and Corporate Officers, irs.gov).

WHY S-CORP REASONABLE COMPENSATION MATTERS

Salary paid to a shareholder-employee is subject to payroll taxes — Social Security and Medicare on the wages (15.3% combined employer/employee up to the Social Security wage base)

Distributions to S-Corp shareholders are NOT subject to payroll tax

This creates an incentive for owners to minimize salary and maximize distributions — exactly what the IRS audits for

Recharacterization of distributions as wages triggers back payroll taxes, penalties, and interest

In Watson v. United States, 668 F.3d 1008 (8th Cir. 2012), the IRS challenged a CPA shareholder's S-Corp compensation. The shareholder, who provided substantial services to his S-Corp, paid himself $24,000 in salary while taking distributions exceeding $200,000 over multiple years. The 8th Circuit Court of Appeals upheld the IRS's recharacterization of approximately $67,044 per year as additional wages subject to payroll tax. The Supreme Court declined to hear the appeal. Watson remains the leading federal authority on S-Corp reasonable compensation and is regularly cited in IRS audits.

Per IRS Fact Sheet FS-2008-25 and the broader case law, the IRS examines the following factors when reviewing whether S-Corp officer compensation is reasonable:

Training and experience of the shareholder-employee

Duties and responsibilities performed

Time and effort devoted to the business

Dividend distribution history (regular distributions while paying minimal salary is a red flag)

Payments to non-shareholder employees performing similar work

Timing and manner of paying bonuses to key people

What comparable businesses pay for similar services

Compensation agreements

Use of a formula to determine compensation

When the IRS successfully recharacterizes distributions as wages: (1) back payroll tax assessed on the recharacterized amount — 15.3% combined employer/employee share; (2) failure-to-deposit penalties under IRC §6656; (3) failure-to-file penalties on the recharacterized Form 941; (4) interest accruing from the original due date. For an S-Corp with multiple years of low-salary/high-distribution patterns, the combined exposure regularly reaches six figures.

What This Guide Does Not Cover

This guide describes the IRS rules governing S-Corp qualifications and limitations as facts. It does NOT cover: (1) whether S-Corp election is the right entity choice for your specific business — that decision depends on projected profit, distribution needs, exit strategy, and state tax rules, and is a separate analysis we addressed in our C-Corp vs S-Corp facts and strategy guides; (2) state-level S-Corp rules — California, for example, imposes a 1.5% franchise tax on S-Corp net income (minimum $800) in addition to federal treatment, and other states have different rules; (3) the mechanics of converting from C-Corp to S-Corp, which has its own set of IRC rules including the built-in gains tax under IRC §1374 for the first 5 years post-conversion; (4) the procedural process for revoking an S-Corp election or curing an inadvertent termination through Rev. Proc. 2022-19 relief; (5) advanced trust planning involving QSSTs, ESBTs, and qualified retirement plan ownership of S-Corp stock; (6) IRS Form 1120-S preparation, basis tracking, or shareholder K-1 reconciliation. Each of these topics requires personal analysis when applied to your specific business.

Where to Go From Here

If you currently operate as an S-Corp, the S-Corp qualifications and limitations under IRC Section 1361 require ongoing monitoring — not just attention at election time. A change in shareholder residency status, a new family-member shareholder, an inadvertent stock transfer, a disproportionate distribution, an undocumented shareholder loan, or a year of underpaid S-Corp officer compensation can each cause significant tax exposure. Working with the right tax planning firm Irvine business owners trust for ongoing S-Corp compliance is the difference between catching a problem early and discovering it during an IRS audit. Tax Wealth Consultant is an Enrolled Agent tax planning firm Irvine based, serving business owners across Orange County and California. Our team reviews S-Corp shareholder composition against the S-Corp 100 shareholder limit, audits compliance with the S-Corp one class of stock rule, evaluates pro rata share S-Corp allocations on Schedule K-1 Form 1120-S, and tests S-Corp reasonable compensation documentation against Watson v. U.S. and IRS Fact Sheet FS-2008-25 standards — bringing your S-Corp into full compliance before the IRS audits the same questions.

Related:

Sources cited in this article: • Internal Revenue Code §1361 — S Corporation defined; small business corporation • Internal Revenue Code §1361(b)(1)(A) — 100 shareholder limit • Internal Revenue Code §1361(b)(1)(B) — Eligible shareholder types • Internal Revenue Code §1361(b)(1)(C) — Nonresident alien shareholder prohibition • Internal Revenue Code §1361(b)(1)(D) — One class of stock requirement • Internal Revenue Code §1361(b)(2) — Ineligible corporations • Internal Revenue Code §1361(c)(1) — Family aggregation rule • Internal Revenue Code §1361(c)(2) — Qualified trusts as shareholders • Internal Revenue Code §1362 — S-Corp election, revocation, and termination • Internal Revenue Code §1366 — Pro rata allocation to shareholders • Internal Revenue Code §1367 — Stock basis adjustments • Internal Revenue Code §1368 — Distribution rules • Internal Revenue Code §1374 — Built-in gains tax • Internal Revenue Code §6699 — S-Corp late filing penalty • IRS Form 1120-S — U.S. Income Tax Return for an S Corporation • IRS Form 2553 — Election by a Small Business Corporation • IRS Schedule K-1 (Form 1120-S) — Shareholder's Share of Income, Deductions, Credits • IRS Schedule K-1 (Form 1120-S) Instructions • Treasury Regulation §1.1361-1(l) — One class of stock rules • IRS Fact Sheet FS-2008-25 — Wage Compensation for S Corporation Officers • IRS, S Corporation Employees, Shareholders and Corporate Officers — irs.gov/businesses/small-businesses-self-employed/s-corporation-employees-shareholders-and-corporate-officers • Revenue Ruling 74-44 — S-Corp reasonable compensation • Revenue Ruling 59-221 — S-Corp shareholder employee status • Revenue Procedure 2013-30 — Late S-Corp election relief • Revenue Procedure 2022-19 — Taxpayer assistance for S-Corp issues • Revenue Procedure 2025-32 — 2026 inflation-adjusted items (including $255 §6699 penalty rate) • Watson v. United States, 668 F.3d 1008 (8th Cir. 2012) — S-Corp reasonable compensation • Glass Blocks Unlimited v. Commissioner, T.C. Memo 2013-180 — Shareholder loans recharacterized |

Want to Know If Your S-Corp Is Actually Compliant?

Tax Wealth Consultant reviews S-Corp shareholder composition under IRC §1361, audits compliance with the S-Corp one class of stock rule, tests reasonable compensation documentation against Watson v. U.S. standards, and verifies Form 2553 election validity. We coordinate the documentation needed to keep your S-Corp election alive and defensible. No sales pitch — just a real analysis.

Or call (949) 409-8335 — speak with an Enrolled Agent Irvine today

Or email support@taxwealthconsultant.com

Comments